We all know our taxes support social security and welfare, such as aged care pensions, family tax benefits and childcare subsidies. They also fund critical infrastructure like roads, public transport systems, hospitals and schools.

As it’s now mid-2021 and as the pandemic rages on, many companies and small businesses continue to struggle. When the new financial year began and the 2021 Federal Budget company tax cut finally kicked in, there was a collective sigh of relief.

With tax matters now high on many a business (and accounting) agenda, you may be wondering just how does taxation affect my business decisions?

Company tax in 2021, 2022 and beyond

It's essential to understand how corporate taxes work in Australia because companies contribute a whopping 19 percent of all Australian taxes. This places them second only to personal income tax as the country’s largest revenue raising sector.

While we won’t go over everything already written, in a nutshell:

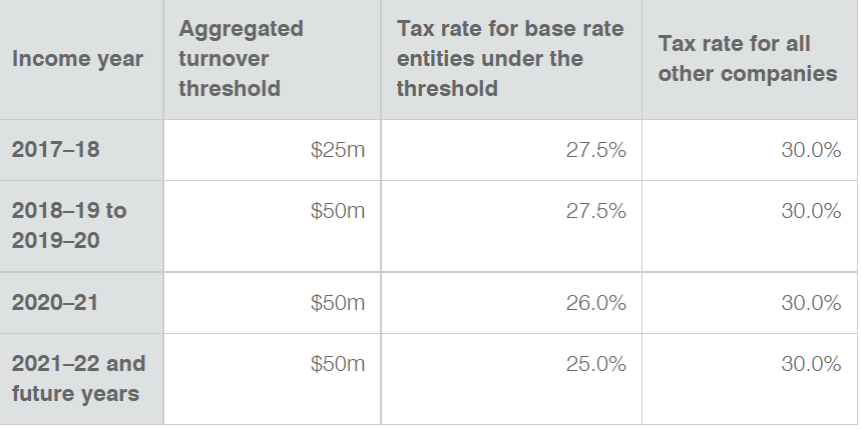

Tax cut - the corporate tax rate for small business (SME) dropped from 27.5 percent to 25 percent from 1 July, 2021.

Company tax rate – according to the ATO website, ‘the full company tax rate of 30% applies to all companies that are not eligible for the lower company tax rate. Eligibility for the lower company tax rate applies if you’re a base rate entity from the 2017–18 income year and onwards.’

Source: ATO Changes to company tax rates page

However, when you’re a business, taxation isn’t as simple as handing over 25 or 30 percent of your income and it’s done. (But this is one excellent reason why working with a financial advisor will ensure you’re getting taxed correctly.)

Taxes can affect your business decision making in any number of ways.

Business Structure

The type of business structure you choose comes with big tax implications. Australia has four main business structures, each with its own set of pros, cons and taxation requirements.

Sole trader

Registering as a sole trader is the quickest, easiest and most common way to set up a business in Australia.

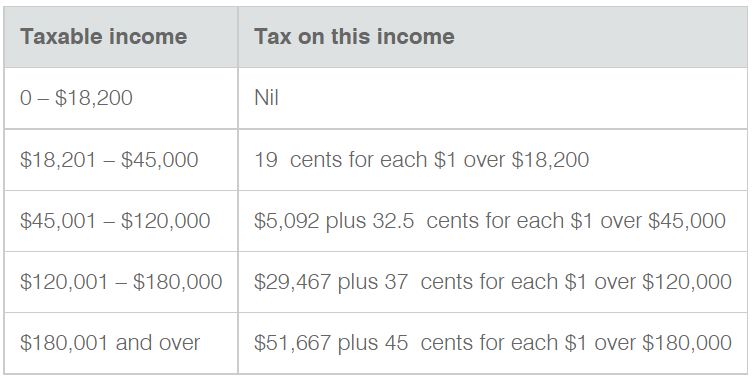

You choose and register a business name, get an ABN and you’re on your way. Sole traders pay tax at the individual tax rate and only need to lodge an individual tax return. The table below is for resident tax rates and doesn’t include the 2 percent Medicare levy.

Source: ATO https://www.ato.gov.au/rates/individual-income-tax-rates/

When you’re a small business, it’s tempting to go down the DIY route. But there’s lots of ways to minimise tax and using an accountant can help you find them.

Partnership

A partnership is when two or more people decide to work together in business.

A partnership structure is still pretty easy and inexpensive to set-up but keep in mind partners can be held personally responsible for business debts. If your partner doesn’t pay, you’re stuck with the debt.

Also, there’s more to consider than being a sole trader. Just a few things the ATO says:

‘the partnership has its own TFN and must lodge an annual partnership return showing all income and deductions of the business’ and

the partnership doesn't pay income tax on the profit it earns – each partner reports their share of the partnership income in their own tax return.’

Company

There’s no tax-free threshold for companies. And as mentioned above, the full company tax rate is 30 percent. However, as of 1 July, 2021, some may only have to pay 25 percent.

Many successful sole traders may be advised to think about changing their business structure when their taxable income is more than 30 percent. Taking the leap from sole trader to company is one way taxes definitely affect business making decisions.

Trust

A trust distributes income to its beneficiaries, such as family members, on lower tax rates. The beneficiaries then declare this income on their own individual tax returns. However, all income must be distributed otherwise, it’s taxed at the highest marginal tax rate of 45 percent.

Goods and Services Tax (GST)

Even if you’re only operating as a sole trader, you may need to register for GST if:

- turnover is more than $75,000 in any 12 month period

- you offer a ride sharing or taxi service.

If you’re a not-for-profit (NFP), you only need to register for GST when turnover is more than $150,000 in any 12 month period.

Currently taxed at 10 percent, GST is passed onto your customers.

However, even if you’re not earning more than the $75,000 threshold, you can still register for GST. Take a look at some of the pros and cons.

Pros:

- you’ll be ready when your turnover does reach the $75,000 threshold.

- you can claim GST credits on the goods and services you’ve bought for your business.

- GST is payable quarterly so this extra money can help with cash flow. But you must have the money available when your Business Activity Statement (BAS) is due, so this can easily become a con if you’re not careful.

- it may make you look more professional. It shouldn’t make a difference, but it does. Charging GST signals your business turnover is more than $75,000, even if that’s not quite true (yet).

Cons:

- once registered, you have to complete a BAS each quarter.

- if you don’t use accounting software, or have an accountant, this can be confusing and time consuming.

- you have to charge GST. This may have some effect on other small businesses you work with if they can’t offset your GST charges.

Growing your business

Many businesses get to the point when they have to decide if they want to grow. Perhaps the sole trader is now working past their capacity. Or the small partnership has expanded.

This may mean increasing prices, employing staff, renting an office or workspace. It may even mean changing the structure of their business.

Whatever business decisions you need to make or however many tax implications you need to consider, the team at Kelly+Partners are with you all the way. So book a discovery session today to see how your business can be better off.

Share this

Presidential Candidates on Taxes

Pay up or shut up shop