The age of retirement seems like a mythical, magical world filled with days of glorious nothingness.

You can read all the books, walk all the walks, see all the things. And you can do it at your own leisure. You no longer have to be anywhere or do anything you don’t want to do.

But much like everything else in life, a financially secure retirement doesn’t just happen overnight.

Whether you’re decades away from leaving paid employment or it’s just around the corner, it’s never too early to start thinking about how to financially plan for your retirement and future.

What’s the retirement age in Australia?

There’s no fixed retirement age in Australia but the Australian Bureau of Statistics (ABS) reports that the average retirement age is 55.4 years.

Some other interesting retirements stats from the ABS:

- There were 3.9 million retirees as at the 2018-2019 financial year.

- 55% of people over 55 were retired, up from 53% in 2016-17.

- Half a million people intend to retire within 5 years.

- The average age people intend to retire is 65.5 years.

- The pension was the main income source for most retirees.

- In 2018-19, 55% of retirees were women.

- The population of retired women increased more than men.

- On average, women retire sooner than men.

It’s interesting to note that while the average age of retirement is 55.4 years, most people don’t intend to retire until they’re 65.5 years old. That’s ten years earlier than planned.

While there could be many reasons why someone would retire a full decade earlier than expected what it tells us is that you need to start planning for the unexpected.

The Aged Pension and other government allowances

The ABS stats tell us that the main source of income for most retirees was a pension. It didn’t state what sort of pension but it’s safe to assume for many, that would be the Aged Pension. Together with savings and superannuation, and depending on your personal circumstances, the aged pension could be a key part of your retirement income.

At what age can you claim the Aged Pension?

The tables below show that most people heading for retirement from July 2023 onwards, are entitled to the aged pension at 67 years of age.

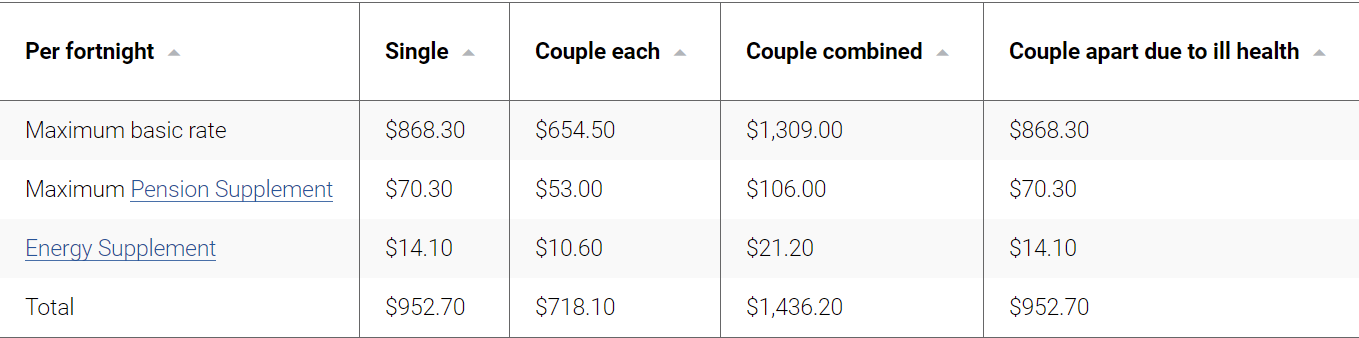

How much is the Aged Pension?

The table and information below are provided without assets and income testing and those amounts need to be considered. As many retirees may in fact end up self-funded and not be entitled to the maximum rate of aged pension. Working with a qualified financial planner such as our team at Kelly+Partners can help ensure your exact circumstances are taken into account when working out what your retirement income might look like.

Depending on your circumstances, you or your partner may also be entitled to a Carer’s Allowance or the Disability Support Pension.

Superannuation - preservation age and accessing your super

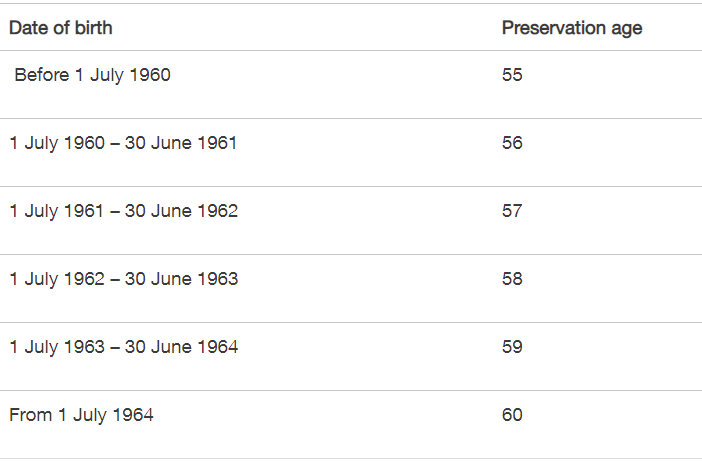

Your superannuation is intended to help fund your retirement and can have a significant impact on your retirement financial planning. You can usually only draw on your super when you reach the ‘preservation age’, which is between 55 and 60 years. But this depends on when you were born.

And while you can start accessing your super once you reach the preservation age, you won’t have full access to it as a lump sum until you meet a condition of release. These conditions include:

- Reaching your preservation age and fully retiring

- Turning 60 and ceasing employment after age 60.

- Turning 65 (even if you’re still working).

- There are some special cases where you may be able to withdraw your superannuation early.

When you start accessing super, which is typically tax-free once you’re 60, there’s a few things you can do with the funds.

Transition to Retirement (TTR)

Once you’ve reached the preservation age, you can supplement your income with a TTR pension. This means you can keep working full time or part time.

Take the money and run!

When you’re ready to retire, you can take your super as a lump sum or choose to set up a pension or annuity to have a regular income.

Tax implications will be different for everyone, so this is a great time to seek professional financial advice.

How much do I need to retire comfortably?

Again, this will depend on the retirement lifestyle that you want. If you plan to travel the world (COVID travel restrictions notwithstanding) you’ll need much more money than someone who’s idea of a dream retirement is sitting on a local beach reading their favourite novels.

As we shared in our article about how much you'll need to comfortably retire, the general rule of thumb is you’ll require about two-thirds (67%) of your pre-retirement income to maintain the lifestyle to which you’ve become accustomed.

The Association of Superannuation Funds of Australia (ASFA) defines the differences between a modest retirement lifestyle and a comfortable retirement lifestyle. It notes:

A modest retirement lifestyle is considered better than the Age Pension, but still only able to afford fairly basic activities.

A comfortable retirement lifestyle enables an older, healthy retiree to be involved in a broad range of leisure and recreational activities and to have a good standard of living through the purchase of such things as:

- household goods,

- private health insurance,

- a reasonable car,

- good clothes,

- a range of electronic equipment, and;

- domestic and occasionally international holiday travel.

The budget for various households and living standards are for those aged around 65 years. The budget assumes that the retirees own their own home outright and are relatively healthy.

Life Expectancy in Australia

ABS figures released in November 2020 show that life expectancy in Australia continues to increase, with a girl born today expected to live to 85.0 years and a boy to 80.9 years. The report continues:

Today an Australian male aged 50 years can expect to live another 32.9 years, and a female another 36.3 years. ‘This is longer than life expectancies at birth, as most 50 year olds have successfully made it through the first several decades of life’.

So, a 50 year old man can expect to live till he’s 82.9 years old. A female until she’s 86.3 years.

There’s a lot of years between retiring at 65 and the average life expectancy. Another sobering reason why it’s never too early to start to financially plan for retirement.

Whenever you choose to retire and however you choose to spend your well-earned retirement, we want to help you be better off. Whether you’ve just started your first job or you’re startled at how quickly retirement is approaching, we’re just a phone call away.

Already a Kelly+Partners Client? Get in touch with your Client Director today!

Share this

.png)

What is a transition to retirement income stream?

Retirement Planning - Top 5 things to think about for your retirement

.png)

%201.webp?width=1920&height=809&name=James%20Howard%20Building%201%20(1)%201.webp)