You might also be surprised to learn that government talk around retirement incomes and superannuation has been around since Federation. However, it wasn’t until 1992 that the Superannuation Guarantee (SG) was announced, stating all employers would need to contribute to superannuation funds on behalf of their employees.

And over the last (almost) 30 years, a lot has changed in the world of superannuation. This includes valid reasons for you to be able to access your superannuation before retirement.

What's Superannuation and the Superannuation Guarantee (SG)?

The Australian Taxation Office (ATO) tells us:

Super, or superannuation, is important because the more you save, the more money you will have in retirement. Super is a long-term investment which grows over time.

For most people, super begins when you start work and your employer starts paying a percentage of your salary or wages into a super fund account for you.

Your super fund invests and manages this money for you until you retire.

The Superannuation Guarantee (SG) is the minimum amount your employer must contribute towards your superannuation. As of July 1, 2021, it was increased to 10 percent with small yearly increases expected until it reaches 12 percent in 2025.

Source: ATO

You can also contribute extra towards your superannuation. All that compound interest can really add up over 30, 40 or 50 years! But as there’s tax implications, we suggest chatting with your financial advisor first.

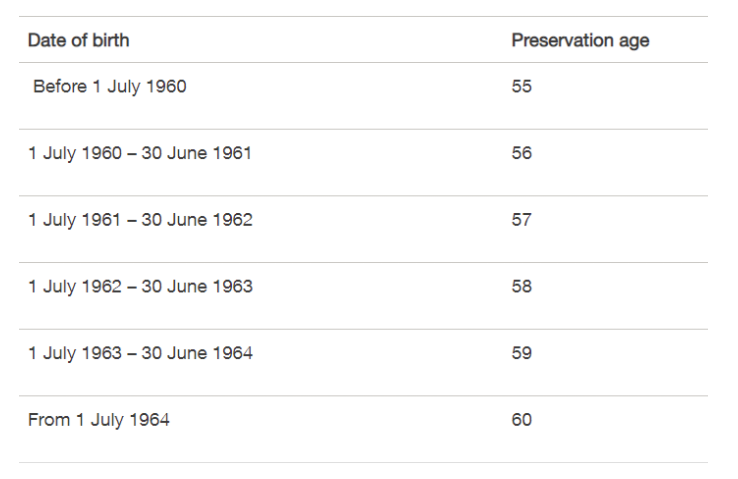

What's the superannuation preservation age?

As your super is meant to be used for your retirement, you can’t access it until later in life. This is known as the ‘preservation age’ and while you can access your super somewhere between the ages of 55 and 60, the actual year depends on when you were born.

And even once you reach your preservation age, there’s still some conditions of release. To access your super as a lump sum, you must meet one of the following criteria:

- Reach your preservation age and retire completely, or

- Turn 60 and stop work for good, or

- Turn 65 (even if you’re still working).

Once you begin to access your super, it’s typically tax-free after 60 years of age.

However, there are special circumstances, called ‘early release’, under which you may be able to withdraw your super early.

Compassionate grounds

You can request to withdraw your superannuation on compassionate grounds for unpaid expenses when there’s no other way to pay them. There are strict limits and you can only withdraw what you absolutely need.

According to the ATO, compassionate grounds includes needing money for:

- medical treatment and medical transport for you or your dependant

- making a payment on a home loan or council rates so you don't lose your home

- modifying your home or vehicle to accommodate your or your dependant's severe disability

- palliative care for you or your dependant

- expenses associated with the death, funeral or burial of your dependant.

As you can see, the conditions are strictly limited and whatever you withdraw is treated and taxed as any other superannuation lump sum withdrawal. Again, as there’s tax implications, please speak to your financial advisor before accessing your super in this way.

Terminal medical condition

The ATO advises, if you’re diagnosed with a terminal medical condition and meet all the following conditions, you can access your super early.

- Two registered medical practitioners have certified, jointly or separately, that the person suffers from an illness or an injury that is likely to result in the death of the person within 24 months of the date of the certification.

- At least one of the registered medical practitioners is a specialist practising in an area related to the illness or injury suffered by the person.

- The 24 month certification period has not ended.

Severe financial hardship

Severe financial hardship isn’t determined by the ATO but by your superannuation provider. You’ll need to contact them to request to withdraw your super early but you must meet both these conditions:

- You’ve received eligible government income support payments continuously for 26 weeks.

- You’re not able to meet reasonable and immediate family living expenses.

If you’re permitted to withdraw some super, the minimum amount is $1,000 and the maximum $10,000 and you can only withdraw once in any 12 month period. If your super balance is less than $1,000, you can withdraw the lot.

Temporary resident and permanently leaving Australia

If you’re a temporary resident and have earned super while working in Australia, you can apply to claim back your super as a departing Australia superannuation payment (DASP).

Permanent incapacity or temporarily unable to work

You might be able to access your super early is you’re permanently incapacitated or temporarily unable to work.

Permanently incapacitated - this type of withdrawal is known as a 'disability super benefit' and is determined by your super fund. The ATO says:

Your fund must be satisfied that you have a permanent physical or mental medical condition that is likely to stop you from ever working again in a job you were qualified to do by education, training or experience.

You can receive the super as either a lump sum or as regular payments (income stream).

Temporarily unable to work – this type of release is used to access your super fund’s insurance benefits. You’ll receive the benefits as a regular income stream if:

You’re temporarily unable to work, or need to work less hours, because of a physical or mental medical condition.

The First Home Super Saver Scheme

If you’re saving to buy your first home, you might be able to access your super under the First Home Super Saver Scheme (FHSSS). According to MoneySmart:

The scheme allows you to make voluntary super contributions to your super account to save for your first home. You can then apply to access those contributions and their earnings to buy your first home.

Eligibility criteria and savings limits apply.

While a few of the reasons to access your superannuation before retirement aren’t very pleasant, it’s good to know, under certain circumstances, you can.

If you have any questions about accessing your superannuation or the tax implications of doing so, please contact your local Kelly+Partners office today. You can also request a call back at a time that suits you.

This offer for Private Wealth Services is not available to clients of BMF as at 31 December 2016.

DISCLAIMER

Kelly Partners Private Wealth (Wholesale) Pty Ltd is a corporate authorised representative of Kelly Partners Private Wealth Pty ltd (AFSL: 516704, ABN 14 629 559 860). Any general advice provided has been prepared without taking into account your objectives, financial situation or needs. Before acting on the advice, you should consider the appropriateness of the advice with regard to your objectives, financial situation and needs.

Kelly Partners Private Wealth Sydney Pty Ltd is a corporate authorised representative of Madison Financial Group Pty Ltd (AFSL: 246679, ABN: 36 002 459 001)

Share this

How to use debt to build wealth

Spring clean your finances