Nobody likes paying taxes.

But making sure you understand your corporate tax obligations is critical to any business. And the start of a new financial year is when many people make their big move when it comes to business changes, such as restructuring.

You might want to keep reading if you thought the 2021-22 financial year was:

- a great time to start a new company,

- the best moment to change your small business structure from sole trader to company, or

- the perfect time to finally understand exactly what’s going on when you speak to your financial advisor or accountant.

Understanding how corporate taxes work right from the beginning will save you headaches later on down the track.

What are corporate taxes?

A corporate tax, also known as company tax, is the tax a government wants paid on the income of a company. Currently, the full company tax rate is 30 percent.

Taxes are important revenue raisers used to finance government activities and, after personal income tax, company taxes make up 19 percent of Australian Taxes.

However, due to the coronavirus pandemic and it’s continuing effects on the Australian economy, the Australian Bureau of Statistics (ABS) reported in late April, 2021:

‘Company income tax was down $7.1 billion (-7.5%) as a result of the adverse effect of the COVID-19 pandemic on businesses with the largest falls in the tourism, banking, superannuation and insurance sectors.’

What this means is that understanding how corporate tax in Australia works is more important than ever.

The 2021 Federal Budget and company tax

When the 2021 Federal Budget was handed down, its goal was to continue to support and stabilise the Australian economy, still dealing with the pandemic. Along with a number of measures we discussed a few months back, it contained a company tax cut.

From 1 July, 2021, the corporate tax rate for small business, or SME, dropped from 27.5 percent to 25 percent.

How do corporate taxes work in Australia?

According to the Australian Taxation Office (ATO) website:

Company tax rates apply to:

- companies

- corporate unit trusts

- public trading trusts.

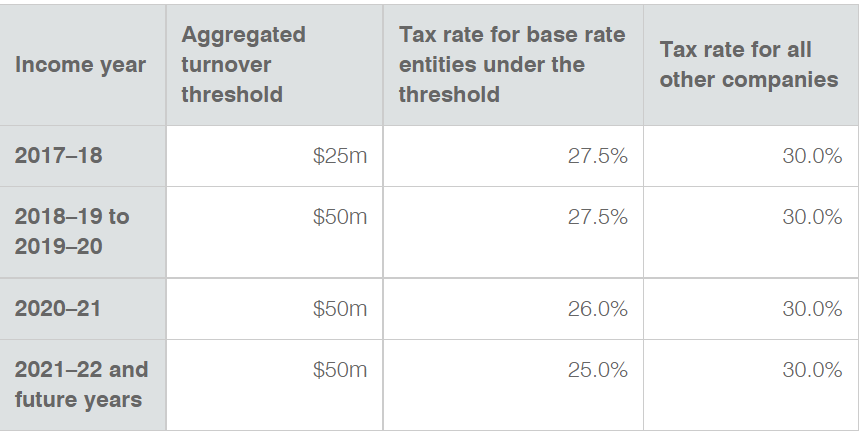

The full company tax rate of 30% applies to all companies that are not eligible for the lower company tax rate. Eligibility for the lower company tax rate applies if you’re a base rate entity from the 2017–18 income year and onwards.

For tax years prior to the 2017-18 income year, the small business entity applied.

What is a base rate entity?

A base rate entity has both:

- an aggregated turnover less than the threshold of $25 million for the 2017–18 income year and $50 million for the 2018–19 income year

- 80% or less of their assessable income is base rate entity passive income, replacing the requirement to be carrying on a business.

Base rate passive income is:

- corporate distributions and franking credits on these distributions

- royalties and rent

- interest income (some exceptions apply)

- gains on qualifying securities

- a net capital gain

- an amount included in the assessable income of a partner in a partnership or a beneficiary of a trust, to the extent it is traceable (either directly or indirectly) to an amount that is otherwise base rate entity passive income.

Source: ATO‘ changes to company tax rates’ page

Company taxes

Corporate tax in Australia is a complicated business and involves more than just taxing 30 percent of a company’s profits. The ATO tells us:

‘The policy underpinning Australia’s tax laws generally means that Australian companies only pay tax on their Australian profits (active and passive) and their foreign passive profits.’

In fact, here are some of the surprising ways in which companies are taxed.

Profits

Okay, not so surprising but how profits are taxed depends on the company's tax rate:

- 25 percent – base rate entities

- 30 percent – all other companies

Goods and Services Tax (GST)

GST is currently 10 percent and added to the supply of certain goods and services. The tax is typically added to your prices and passed onto your customers.

Your company must register for GST when:

- turnover is more than $75,000 in any 12 month period

- you offer a ride sharing or taxi service

- you’re a not-for-profit (NFP) and turnover is more than $150,000 in any 12 month period.

Capital Gains Tax (CGT)

A company may pay CGT when selling a company asset outside the ordinary course of its business (for example, property). The capital gain is calculated as the difference between what the company paid for the asset and for how much it was sold.

Fringe Benefits Tax (FBT)

FBT is an employer tax on benefits they provide to an employee, other than a salary. This can include things such as gym memberships, E-tags, employee vehicle, home phone or internet etc.

Distinct from company income tax, the FBT years runs from 1 April to 31 March. Calculated on the actual fringe benefit, it’s a self-assessed liability and requires a separate FBT return to be lodged.

The current FBT rate is 47 percent.

As you can see, corporate taxes can quickly become complicated. This is why sound, professional financial advice is not a suggestion when it comes to company taxes, it’s a must-have.

If you’re keen to understand your company's tax obligations, and even more keen to pay less tax, book a discovery meeting to learn ways to keep you and your company on the good side of the tax office.

Share this

-1.png)

Do you pay taxes on inheritance in Australia?

2023 Year End Tax Planning Guide

%201.webp?width=1920&height=809&name=James%20Howard%20Building%201%20(1)%201.webp)