Warren Buffet once said of the power of compounding:

"Life is like a snowball. The important thing is finding wet snow and a really long hill".

This is a nod to the combination of both time and compound interest in increasing wealth.

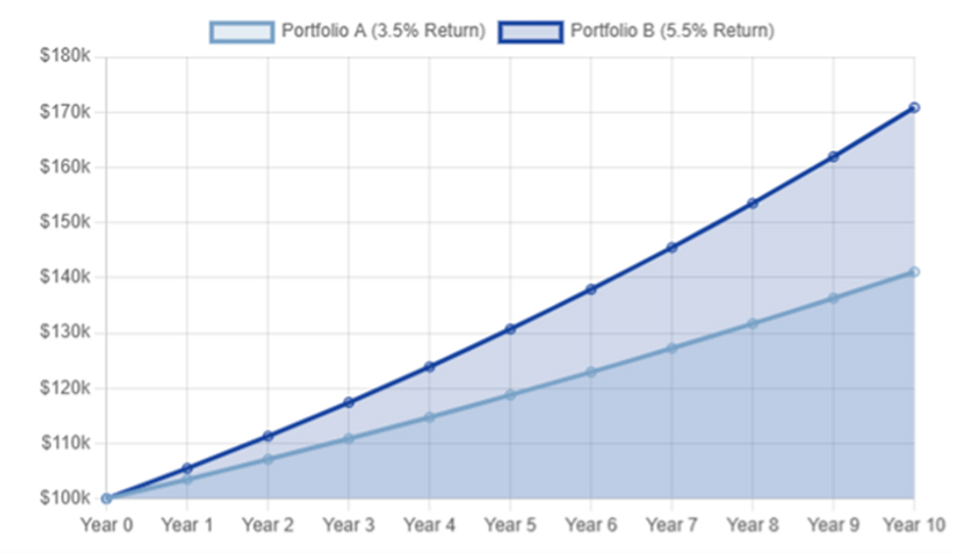

An investment strategy that achieves a sustained 2%+ annual return premium can create a significant difference in long-term wealth accumulation. For example, the comparison of a $100,000 portfolio reveals that a 5.5% annual return, compared to a 3.5% annual return, generates an additional $29,754 over a 10-year investment horizon. This substantial difference is not a simple linear gain but rather due to the exponential power of compounding.

The pursuit of this return premium, however, requires a deliberate shift in investment strategy. With the Reserve Bank of Australia's (RBA) cash rate at 3.6% (and market expectations pointing towards further reductions), a target return of 5.6% or higher may require investors to consider a different approach to their asset allocation and risk profile.

Even a seemingly small 2% difference in annual returns can create a substantial gap in portfolio value over a decade. Let's look at how an initial $100,000 investment grows in two different scenarios:

After 10 years, the higher-performing portfolio not only grew more, but the difference in total earnings becomes a significant amount, highlighting the long-term cost of lower returns.

- Portfolio A (3.5% p.a.)

$141,060 - Portfolio B (5.5% p.a.)

$170,814 - The 2% Difference

$29,754

The RBA Cash Rate and the Risk-Return Trade-Off

The investor's goal of achieving a 2% premium above the current cash rate implies a target annual return of 5.6%. However, this is not a static benchmark. Financial markets, as reflected in the ASX 30 Day Interbank Cash Rate Futures, anticipate further rate cuts. Major banks also forecast a decline, with some predicting the cash rate could fall to 3.10% or even 2.85% by early to mid-2026. The RBA's own forecasts for private demand are conditioned on a cumulative 80 basis point easing in the cash rate over the coming year, which would support economic growth.

This dynamic environment presents a critical challenge for the investor. As the RBA's cash rate falls, the "risk-free" rate of return and the return on assets like cash and term deposits will also likely diminish. Consequently, an investor seeking to maintain that 2% premium would need to take on a higher level of risk to compensate for the diminishing returns from low-risk assets. This situation reframes the entire problem, transforming it from a static calculation into a dynamic investment strategy that must continually adapt to the changing economic climate.

The Hazards of Yield Chasing

The pursuit of a higher yield, such as the 5.6%+ target, can lead investors to focus on a single metric while ignoring crucial underlying fundamentals. This is a behavioural trap known as "yield chasing," and it can result in exposure to significant and often-overlooked risks.

Additionally, investors seeking a premium return must be aware of several other, more systemic, forms of risk.

To achieve a return of 5.6% (2% above the RBA cash rate of 3.6%), investors typically need to move beyond cash and term deposits, embracing assets that carry higher potential returns but also greater risk. The key is to find a balance that aligns with your personal goals and risk tolerance.

As CEO and the fund’s portfolio manager at iPartners, Travis Miller, notes: “There is strong demand for a fund covering cash, term deposits and private credit assets amid the increasingly volatile markets around the world.

Managing Partner at Kelly+Partners Private Wealth, Trent Doughty, said “We are offering a monthly distribution and redemption feature in some of our fund offerings so our investors can be nimble, while securing their funds in a relatively safe harbour for six months or longer.” For wholesale investors (individuals with a gross annual income of greater than $250,000 for the past two years or net assets in excess of $2.5 million), the Core Income Income Fund has been designed to deliver a higher yielding portfolio of private credit and fixed income assets.

The iPartners Core Income Fund, targets an interest rate of 7% per annum, maintaining a holding in a selection of credit assets, fixed income and managed funds. The fund is designed to provide monthly applications, distributions and redemption feature, with a view to provide a stable income yield.

To learn more, please contact Kelly+Partners Private Wealth at: investments@kellypartners.com.au

Source: iPartners

Share this

Japan's Economic Revival: A Bright Spot for Global Investors

Private Credit in Australia vs. USA: A Tale of Two Markets

%201.webp?width=1920&height=809&name=James%20Howard%20Building%201%20(1)%201.webp)