As you approach retirement age, you might be thinking of the day you walk out the door for the last time and never have to work again. However, for some people, full retirement isn’t on the cards. At least, not just yet.

Some people don’t want to retire. What they want to do is have the option to keep working full time or cut down on their working hours without giving up their current lifestyle and income levels.

For those wanting to continue working and ease into retirement without losing income, you might want to consider the transition to retirement (TTR) income stream. However, before making any big decisions, it’s good to understand how much you’ll actually need to comfortably retire.

What’s a transition to retirement income stream all about anyway? And how can you make it work for you?

What is a transition to retirement (TTR)?

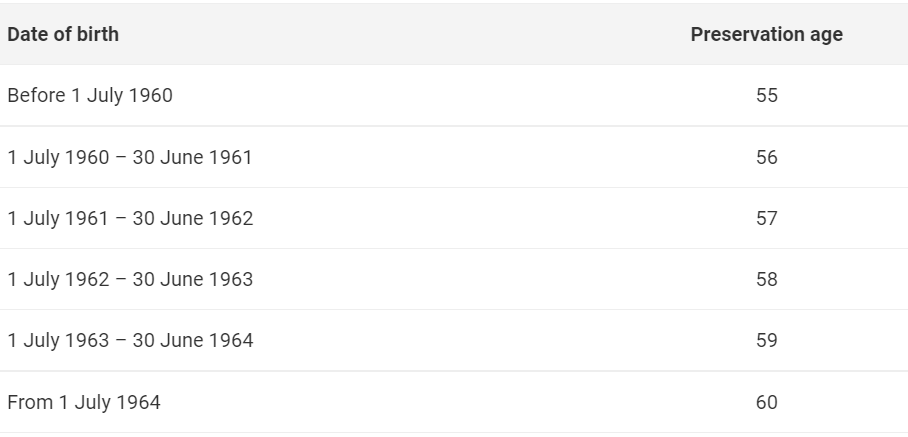

A transition to retirement (TTR) is a scheme that means that once you reach the age of around 55 to 60 years and you’re still working, you can start to use your superannuation to supplement your income. At what age this happens depends on your superannuation preservation age, which is the age at which you can legally access your super. Your preservation age depends on your date of birth.

Using a TTR strategy, that is a transition to retirement income stream (TRIS), lets you boost your superannuation, save tax and keep working. The TRIS may sometimes be referred to as a TTR pension, or pre-retirement pension.

Setting up your TRIS can be a little tricky, so we suggest you discuss it with one of our professional financial advisors.

The changing face of accessing your superannuation

Once upon a time, you could only access your superannuation when you were 65 years old. However, the government changed the rules to allow older Australians to decide how and when they would retire. The Australian Taxation Office (ATO) advises:

‘Under the transition to retirement rules, if you have reached your preservation age, you may be able to reduce your working hours without reducing your income. You can do this by choosing to start a transition to retirement income stream (TRIS).

The TRIS tops up your part-time income with a regular 'income stream' from your super savings…..

Under these rules, you can only access your super benefits as a 'non-commutable' income stream. A non-commutable income stream is one that you can't convert into a lump sum. This generally means you can't take your benefits as a lump sum cash payment while you are still working. You must take your super benefits as regular payments.’

What is a transition to retirement income stream?

As you can see from the ATO page, a transition to retirement income stream (TRIS) is not a way for you to access your super early. While the rules of a transition to retirement income stream are set by the federal government, how a member accesses their funds depends on the fund’s rules. You can usually access your super funds in one of two ways:

Income stream – your super fund pays you a portion of your funds regularly, such as weekly, fortnightly or monthly. In other words, your super fund pays you a pension.

Lump sum payment - a one off payment. It may be all your funds or just a percentage.

You can also access funds both ways by taking some as a lump sum and some as a regular super income stream. But this is something worth checking directly with your super provider, as there may be potential limitations around what you can withdraw as a lump sum. The ATO provides a good overview on the different super withdrawal methods that may be available to you.

How does a transition to retirement pension work?

The Australian Government’s MoneySmart site states ‘you can start a TTR pension by transferring some of your super to an account-based pension’ which offers ‘regular, flexible and tax-effective income from your superannuation.

However, you need to keep some money in your superannuation account to enable you to continue receiving your employer’s compulsory contributions, which increased to 10% on July 1, 2021. You can also still continue to make voluntary contributions to your super fund.

How are the pros and cons of an account based pension?

As the most common transition to retirement income stream, let’s check out some of the pros and cons of an account based pension.

Benefits

- Tax effective – from age 60, you don’t pay tax on pension payments. And if you’re aged between 55 and 59, while the taxable part of your pension is taxed at your marginal tax rate, you’ll get a 15% tax offset on the rest.

- Flexible – you can choose how much you want to be paid

- Aged Pension - if you’re eligible, this can top up your Aged Pension

- Lump sum – you can take it all or just some.

Cons

- Aged Pension – as your account based pension is classed as income, this may affect your government Aged Pension

- Longevity – your super may not last as long as you do.

What is the TRIS retirement phase?

Your TRIS account moves into the retirement phase when a member meets one of the following conditions of release:

- reaches 65 years of age

- retires

- is terminally ill, or;

- becomes permanently incapacitated.

A few things to consider before setting up a transition to retirement income stream

Does your super fund allow you to set up a TTR pension and how will it affect your current or future government entitlements?

Do you want to keep working until retirement? Do you want to stay with your current employer until then, and do you even want them to know you’re considering retiring?

How long until you reach retirement age, how much is in your super fund and will it last until you die?

As you can see, setting up a transition to retirement income stream has a lot of moving parts with many financial implications. If you're interested in seeing how we you can get your wealth to go further, please talk with your Kelly+Partners Client Director. Not a Kelly+Partners Client? Book a Discovery Session today.

Share this

SMSF Investment Strategy for Retirement in a Low Yield Environment

.png)

How to financially plan for retirement

%201.webp?width=1920&height=809&name=James%20Howard%20Building%201%20(1)%201.webp)